The boom in smartphone sales in Africa is slowing, despite the fact that overall mobile handset shipments were up slightly in Q2 2016, with shipments of basic feature phones rising 31.9 per cent year on year to total 29.8 million units.

That’s according to figures from IDC’s recently published Worldwide Mobile Phone Tracker, which also notes shipments of smartphones in Africa fell 5.2 per cent to 23.1 million units in the second quarter of 2016.

Elsewhere statistics from Analysys Mason indicate that the Sub-Saharan Africa telecoms services market will be worth $51 billion in 2021, up from $41 billion in 2015. Mobile services in the region will represent more than 88.4 per cent of the telecoms service revenue in 2021.

Below we’ve outlined 15 stats that explore these and other market drivers in Sub-Saharan Africa. The article originally appeared in MEF’s most recent Africa eBulletin which can be downloaded here for free.

Mobile data, handsets and networks

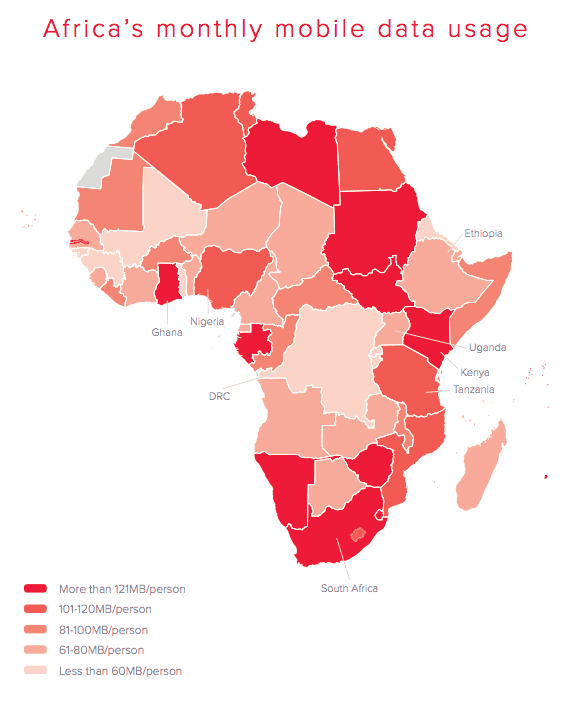

1. According to Research ICT Africa, South Africa’s cheapest 1GB data product places 16 of out 47 African countries. Tanzania has the cheapest 1GB for US$0.89, in comparison to South Africa – priced at US$5.26.

Egypt, Kenya, and Nigeria also have better data prices than South Africa.

2. The GSMA has found that mobile broadband connections accounted for more than a quarter of all connections at the end of 2015. By 2020 that figure will rise to two thirds with 3G being the dominant network technology.

3. A report by Budde Research indicates that Nigeria has Africa’s largest mobile market, with about 150 million subscribers and a penetration rate of 107 per cent.

4. Focussing on South Africa, Budde Research also shows that the mobile sector has become a key driver of the overall market. As well as carrying most voice traffic, mobile networks account for 97 per cent of all Internet connections with SIM card penetration by late 2016 approaching 160 per cent.

5. Euromonitor handset research in South Africa shows that Samsung Electronics led sales of mobile phones in 2016 with a volume share of 46 per cent, followed by Nokia South Africa and Core Computer Business with 16 per cent and 12 per cent respectively.

6. The boom in smartphone sales in Africa is slowing, despite the fact that overall mobile handset shipments were up slightly in Q2 2016, with shipments of basic feature phones rising 31.9 per cent year on year to total 29.8 million units.

That is according to the latest figures from IDC’s recently published Worldwide Mobile Phone Tracker, which also notes shipments of smartphones in Africa fell 5.2 per cent to 23.1 million units in the second quarter of 2016.

7. According to Deloitte’s African Consumer Survey, the offloading of mobile data traffic onto Wi-Fi networks is a growing trend to accommodate growing demand and operators are actively investing in Wi-Fi deployments. In Nigeria its 83% mobile 16% WiFi and in South Africa its 52% mobile and 46% WiFi.

8. The same survey indexed the proportion of consumers using smartphones versus feature phones in urban and rural areas. As you would expect, smartphones are higher in urban areas in all markets surveyed. Interestingly, smartphone, tablet and laptop ownership in rural areas is high in South Africa and Nigeria.

In urban Nigeria the split is smartphone 93%, feature phone 18% and in rural areas it breaks down as smartphone 82%, feature phone 27%. In urban South Africa smartphones account for 99% and feature phones 17%. In rural areas it breaks down as smartphone 83% and 20% feature phones.

Other countries in the study include Kenya, Uganda and Zimbabwe.

Mobile content and services

9. A report by the African Internet Society indicates that around 320 million people in Sub-Saharan Africa and 140 million people in North Africa who are covered by mobile broadband don not use it indicating a need for more localised Internet services in local languages.

10. According to statistics from Analysys Mason, The Sub-Saharan Africa telecoms services market will be worth $51 billion in 2021, up from $41 billion in 2015. Mobile services in the region will represent more than 88.4 per cent of the telecoms service revenue in 2021. It notes this will be driven by population growth, expansion into rural areas and a high demand for mobile data services.

11. Opera’s State Of The Mobile Web Africa report indicates that one third of South Africans use apps, compared with 31 per cent in Ghana, 28 per cent in Nigeria, 19 per cent in Kenya and 18 per cent in Uganda.

12. The same report shows that 42 per cent of South Africans watch video content on mobile.

13. The value of mobile money transactions in Sub-Saharan Africa reached $655 million in 2014 and could surpass $1.3 billion by 2019, according to data from Frost & Sullivan.

14. According to the GSMA at the end of 2015 46 per cent of the population of Africa subscribed to mobile services, equivalent to half a billion people with Egypt, Nigeria and South Africa accounting for one third of the total subscriber base. Over the next five years the regions subscriber base will grow to 725 million by 2020.

15. Nigeria tops the league table of Facebook users in Sub-Saharan Africa, with more than 15 million users, followed by South Africa and Kenya with thirteen and five million users respectively.

Download the free MEF Africa eBulletin now

MEF’s quarterly Africa eBulletin contains the insights, market stats, news and opinion that frame the ever-evolving pan-African mobile ecosystem.

The last issue of this eBulletin series looked at the implications of Africa moving past its billionth mobile subscriber and the roll-out of 3G and 4G networks. This time around we turn our attention to some of the services enabled by these advances, as well as the changing landscape of content and messaging.

MEF Member Srinivas Nidugondi, Head of Mobile Financial Solutions at Mahindra Comviva, outlines some of the enablers and barriers to the adoption of contactless payments by African consumers.

And Karim Yaici, lead analyst for Analysys Mason’s The Middle East and Africa regional research programme, discusses the market drivers in the region forecasting strong growth for data against a backdrop of declining voice revenue.