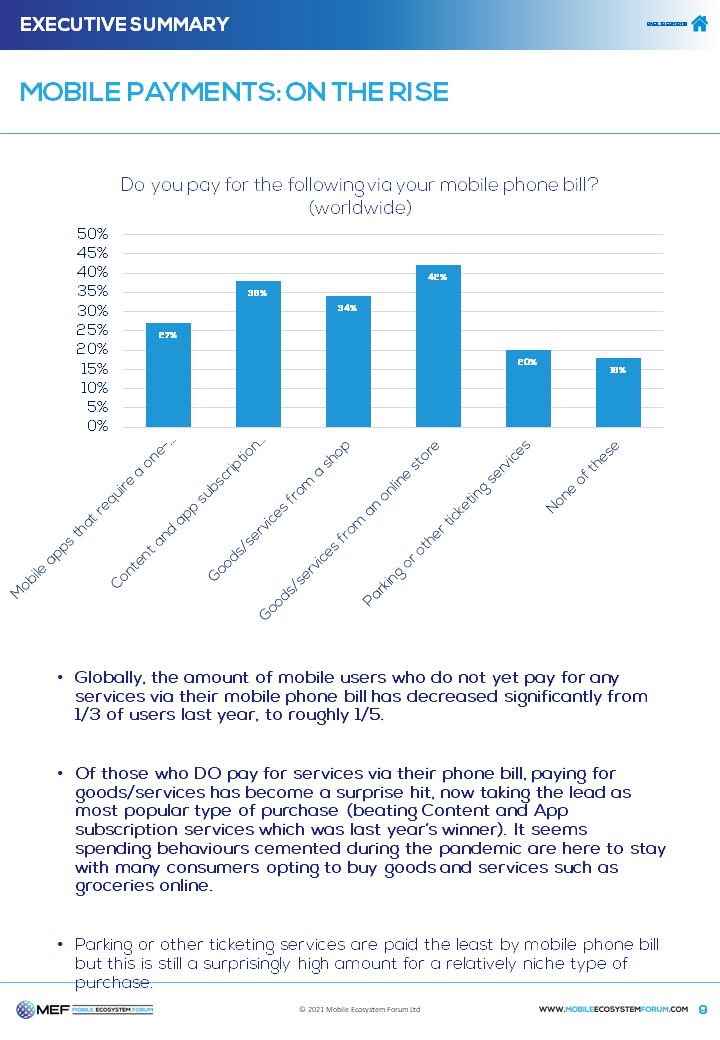

The Payments market is both vast and varied. Nothing stays the same for long and the only REAL barometer of how the industry is truly doing surely can be through speaking to the people whose lives we are attempting to impact – subscribers, consumers – and asking them? Well, this is what we have continued to do here at MEF, year after year. On behalf of MEF, On Device Research surveyed 6,500 smartphone users, 650 in each of 10 markets.

Trust is King

Mention the topic of Mobile Payments and it’s easy for many to fall into the trap of thinking it’s all just about bank transfers, direct debits, debit cards, credit cards and (don’t forget) cash.

But the world of Payments has moved so far beyond that now with so many payment mechanisms now in place.

Whether it’s Mobile Payments through wallets, payment links, QR codes or directly through a mobile phone, the charge being added to the phone bill (DCB, Direct Carrier Billing) or any other mechanism, there are plenty of choices available to enterprises and individuals alike.

The annual survey we commissioned allowed us to take a good look at consumers’ attitudes in Brazil, China, France, Germany, India, Japan, South Africa, Spain, the UK and the USA.

MEMBER DOWNLOADS - REPORT + DATA FILES

This content has been restricted to logged in users only. Please login to view this content.

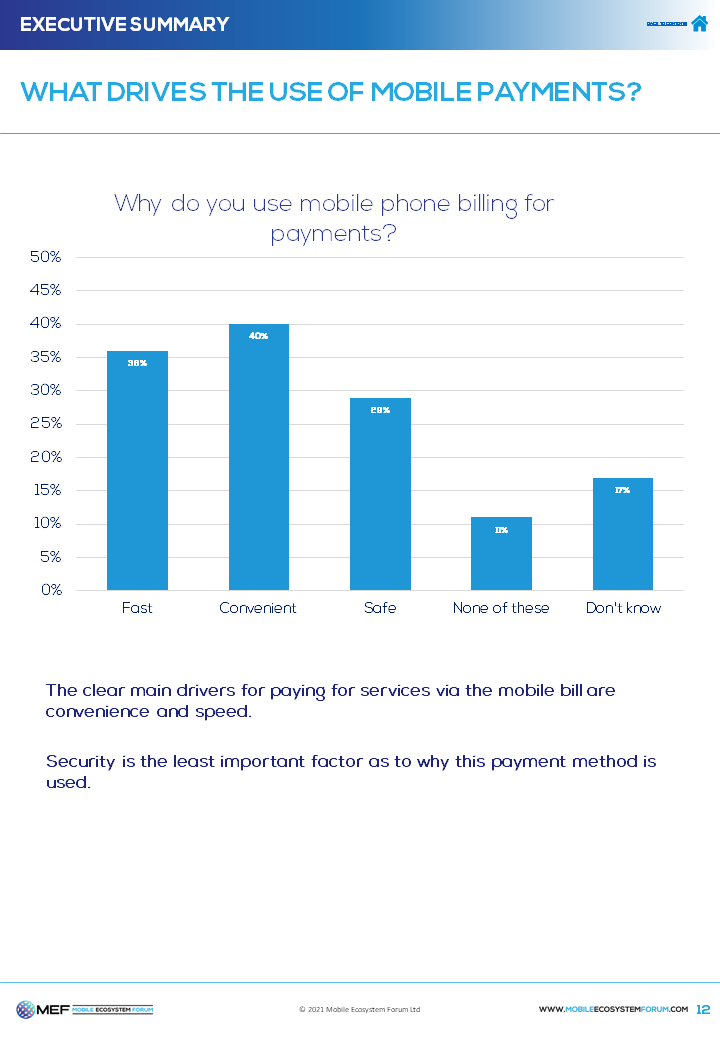

We again got the bottom of what truly motivates their behaviour to pay via different means and throughout there is a visible strand of just how important trust is in a channel to be of huge importance. Of course usability and the customer experience at the end of the day are critical too but if the base starting point is one where the average consumer is (for example) fearful their payment details might be stolen then not being able to change this will seriously negatively impact progress.

With the industry initiatives that exist to attempt to block fraud and spam everywhere, we’d all like to think we are winning the war but the jury is out on that one. The likes of spam are most definitely still out there and collectively we must work together and double down on our efforts to protect consumers everywhere.

Key Findings

-

Consumer Trust Varies Greatly By Country

Those of you who have had details stolen and your online identity compromised will know just how painful it can be to rectify the situation. Fear can be very real and in the report you’ll see just how much concerns vary from one country to another. There is precious little uniformity here.

-

More Work Required To Boost Image Of How Safe Direct Carrier Billing (DCB) Is

Of the payment channels surveyed adding the charge for something to a mobile phone bill was viewed as being the least safe method. Perception is truly important and it’s clear the industry has a lot of work to do to improve sentiment towards DCB. MEF members are definitely doing their bit towards this in our ‘Direct Carrier Billing For Growth’ working group!

-

Issues With Overbilling Remain

On the face of it you would think it should be fairly easy to provide customers with an accurate bill each month but the old issue of overbilling keeps surfacing year after year. On a country basis the number of consumers reporting having incorrect or too many charges on their accounts differed markedly, ranging from 42% to 19%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}